Balancing the Budget on Borrowed Time: NYC’s Pension Shell Game

Short-term savings. Long-term risk. And New Yorkers pay the price.

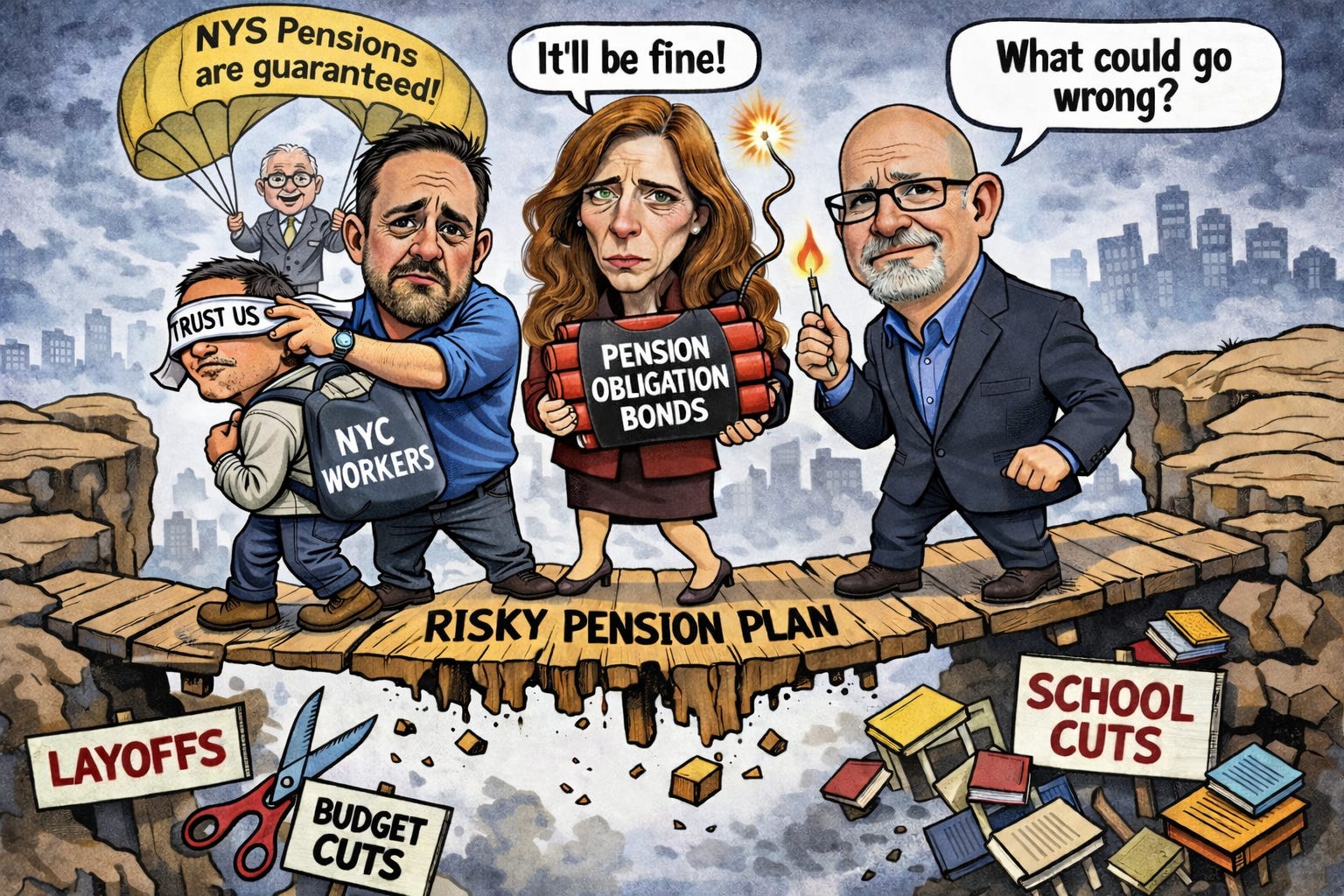

New York City Council’s latest budget proposal isn’t just creative accounting—it’s a high-stakes gamble with workers’ futures dressed up as fiscal responsibility.

Buried inside the City Council’s preliminary budget response is a plan to rely on two controversial tools: re-amortization of pension debt and pension obligation bonds (POBs). Both promise short-term relief. Both come with long-term consequences.

And both are being advanced while union leadership tells members there’s nothing to worry about.

The Plan—In Their Own Words

From the Council’s proposal:

“The City could find substantial savings… that exceed $1.2 billion per year… without impacting a single pension payment.”

And further:

“The first option available is the re-amortization of the current payment schedule…”

“The second option… would be to explore the use of pension obligation bonds (POBs)… The proceeds would then be immediately deposited into the pension funds.”

On paper, it sounds painless: no benefit cuts, no layoffs—just “savings”.

But what’s being described isn’t savings—it’s a restructuring of obligations designed to ease pressure now by shifting it into the future.

All while the City Council acknowledges that there is additional risk.

Re-Amortization: Relief Today, A Longer Tail Tomorrow

Re-amortization, or pension smoothing, works much like refinancing a mortgage. Payments shrink in the short term, but the repayment timeline stretches, and total costs grow.

New York City’s pension system is already structured over long horizons — the City is presently making re-amortization back payments until 2032. Adjusting that schedule again doesn’t eliminate liabilities—it delays them further in volatile economic times. The bill doesn’t disappear; it moves further down the road, where it compounds in interest quietly.

What looks like fiscal breathing room today becomes a longer, heavier burden of taxpayer obligations tomorrow.

Pension Obligation Bonds: Borrowing on Optimism

Pension obligation bonds take that logic a step further. Instead of just reshaping payments, the City would borrow money outright, inject it into pension funds, and rely on investment returns to outperform the cost of borrowing.

If the market underdelivers, the City doesn’t just fall short—it ends up carrying both the original pension burden and the added weight of bond debt. What begins as a strategy to stabilize finances can quickly become a multiplier of risk.

History offers more than theory—it offers warnings.

In Detroit, officials issued roughly $1.4 billion in pension obligation bonds just before the 2008 Financial Crisis. When markets collapsed, the strategy unraveled. Pension investments fell while bond debt remained fixed, leaving the city squeezed from both sides and contributing to its eventual bankruptcy. A similar dynamic played out in Stockton, where pension borrowing collided with a housing market crash and declining revenues, helping push the city into insolvency. In both cases, POBs didn’t create the crisis—but they amplified it at the worst possible moment.

Other governments show how the risks can build more slowly but just as dangerously. Illinois turned to pension obligation bonds in the early 2000s to ease budget pressure, yet decades later remains burdened by some of the worst-funded pensions in the country alongside ongoing debt service. In Puerto Rico, repeated reliance on borrowing to meet long-term obligations contributed to a broader debt spiral that ultimately led to default and federal oversight. The lesson across all four is consistent: borrowing against the future can create the illusion of temporary stability, but it also introduces a layer of risk that becomes most dangerous precisely when conditions deteriorate.

Warnings from Inside the System

A former New York City pension director, retired NYCERS Executive Director John Murphy, warned that proposals like re-amortization may offer immediate budget relief but come at a cost—weakening long-term funding discipline and increasing the likelihood that future obligations become harder to meet. The concern isn’t theoretical; it’s operational. Stretching out payments can erode the structural integrity of the system over time.

That concern was not limited to internal administrators. Former New York City Comptroller Brad Lander (D) and former City Council Finance Committee chair Justin Brannan (D) also warned against a similar re-amortization proposal when it surfaced last year, joining a rare consensus of liberal and conservative fiscal watchdogs, policymakers, and pension experts who viewed the approach as a risky maneuver rather than a real solution.

Analysts across the political spectrum cautioned that the proposal would reduce near-term payments while increasing long-term costs—shifting liabilities forward instead of addressing them.

That same reporting situates these proposals within a broader fiscal pattern. As budget pressures mount, policymakers have increasingly looked toward long-term funds—including the Retiree Health Benefits Trust—as sources of flexibility. But these are not surplus accounts; they are commitments set aside for future retirees. Using them now introduces vulnerability later, particularly in the face of economic downturns.

What emerges is not a one-off decision, but a governing approach: managing present constraints by drawing against the future.

Pizzitola’s Warning: The Illusion of Stability

Her organization, the NYC Organization of Public Service Retirees, was among the first to expose and challenge a similar re-amortization effort last year. According to her reporting, the proposal surfaced with little public scrutiny and would have lowered near-term City contributions by extending pension costs further into the future—effectively refinancing the obligation. What followed was telling: once brought into the open, the plan faced increased resistance and scrutiny, raising questions about how such consequential changes were being advanced with limited transparency.

Her analysis suggests that re-amortization and pension borrowing don’t resolve liabilities so much as reposition them—moving costs outward while relying on favorable conditions to hold. The danger lies in how convincing that can look in the moment. Budgets appear balanced, pressure eases, and the system seems intact.

But the risk is very real. When assumptions about returns, growth, or stability don’t materialize, the burden doesn’t vanish—it reappears, often larger and more urgent. And when it does, it lands on future taxpayers, future budgets, and potentially the very workers whose benefits were said to be untouched.

Her warning is straightforward: a strategy that depends on everything going right is not protection—it is exposure.

Another Warning from Goldstein

Goldstein, who has long written on union and retiree issues and is a potential candidate for leadership within the Retired Teachers Chapter, frames the issue less as technical policy and more as a question of trust. Workers were promised stability in exchange for years of service and concessions. Reworking how those promises are financed—especially without clear, transparent communication—raises concerns that the same pattern is repeating: immediate gains prioritized over long-term security.

A Pattern Taking Shape

Taken together, re-amortization, pension obligation bonds, and the potential use of retiree health funds reflect a disturbing consistent fiscal instinct. Immediate gaps are addressed not by reducing structural imbalance, but by extending timelines and leaning on risking future resources.

It is a strategy that can sustain itself for a time. But it is also one that accumulates pressure beneath the surface, where it is less visible and easier to defer.

The UFT’s Silence—and Its Contradiction

Against this backdrop, the United Federation of Teachers has told members that claims the City is using pensions to balance the budget are a “myth.”

To reinforce that message, union leadership has paraded voices like TRS Chair Tom Brown, who has publicly dismissed concerns as “misinformation” while offering no position, nor educating members about the proposal.

At the same time, others within the pension governance space are telling a very different story. David Kazansky, a nine-year former trustee and current TRS candidate, has been actively working to inform members about the details contained in the City Council’s proposal—pointing directly to the use of re-amortization and pension obligation bonds as mechanisms tied to budget savings.

Concerns are not limited to retirees or outside advocates. Rank-and-file leadership has begun speaking out as well. Brooklyn D75 chapter leader Chad Hamilton put it this way:

“When Mulgrew’s TRS trustee candidate, Tom Brown, says politicians cannot take money from our pension fund, that is technically correct.

However, while politicians cannot take money out, they can absolutely reduce and delay the money going in. This has had disastrous results and contributed significantly to eventual financial insolvency in other U.S. cities and Puerto Rico.

Our union should be having an open dialogue about this important issue. Instead this issue will get a quick and casual mention by Mulgrew at the monthly, Unity-controlled and anti-democratic UFT Delegate Assembly.

Mulgrew will tell us without explanation that anyone with questions or concerns about this plan is a liar and a hater of the union, and then he will move on to the next topic. Many of the Unity caucus sycophants in the audience will clap and cheer, without even knowing what they’re clapping for.

This is the bizarre and disturbing state of our union.”

At the same time, the union is pushing to “fix Tier 6,” advocating for expanded pension benefits that would increase long-term system costs.

The tension between these positions is difficult to ignore. Members are being reassured that pensions are not part of the City’s budget balancing strategy, even as official documents outline over a billion dollars in annual savings tied to pension financing changes—and internal voices raise concerns about what that actually means.

What’s missing is a clear, transparent explanation that reconciles these competing narratives.

Is the silence due to a possible backroom deal to support these financing schemes in return for fixing Tier 6?

Has City Council Speaker Julie Menin promised giving the non-pensionable $10k relief payments for paraprofessionals on the back of pension financing?

The Real Question: Who Carries the Risk?

City officials maintain that these proposals do not affect current retirees or workers. That may be true in the immediate sense.

But it rests on a chain of assumptions: that markets perform as expected, that revenues stabilize, and that future leaders can absorb the deferred costs without consequence.

If those assumptions hold, the strategy works.

But … if strategies like pension obligation bonds fail—if investment returns fall short or costs grow faster than expected—the City is still legally required to meet its pension obligations under the New York State Constitution.

That means the money has to come from somewhere.

In practice, that leaves few options: budget cuts, workforce reductions, or shifts in funding away from core public services. Education—one of the largest areas of City spending—would almost certainly be impacted. Layoffs, program cuts, and reduced resources wouldn’t be hypothetical—they would be likely.

There is no scenario where the obligations disappear. If the risk embedded in these financing strategies materializes, the cost doesn’t vanish—it is redistributed and compounded. And ultimately, it is borne by all New Yorkers.

“It’s a Myth”? The Record—and the Contradiction—Say Otherwise

The UFT has reassured members that claims the City is using pensions to balance the budget are a “myth.”

But the City Council’s own proposal states:

“The City could find substantial savings… that exceed $1.2 billion per year…”

“The first option available is the re-amortization…”

“The second option… would be to explore the use of pension obligation bonds…”

That is the City explicitly identifying pension financing changes as a source of budget savings, which in turn are used to help balance the budget.

So the message to members becomes contradictory:

Pensions aren’t being used to balance the budget. Pensions cannot be raided — unlike Mamdani’s doomsday budget proposal to raid the City’s Rainy Day Fund and Retiree Healthcare Benefits reserve trust fund.

Yet pension financing is being potentially restructured to generate over $1 billion in savings through mechanisms like re-amortization and pension obligation bonds—strategies that shift risk into the future.

No—this isn’t a direct cut to benefits.

But it is a clear use of pension funding structure to reduce current-year obligations.

Calling that a “myth” isn’t clarification or fact-checking.

It’s talking points framing.

And when that framing collides with policies that expand costs while obscuring how they’re managed, it raises a more serious question:

Who is being told the full story—and who isn’t?

Related: